S3 T2 BAFS

Types of enterprises

Private enterprises

- private individuals

- generating profits

- e.g. sole proprietorship, partnership, limited company.

Public enterprises

- wholly owned by government

- provide essential goods and services to the public

- e.g. Ocean Park / Water Supplies Department

Legal Entity & Limited Liability

Firm -> not a separate legal entity

- no separate legal existence from its owner

- owners enter into contracts, sue, and being sued.

- closed upon withdrawal/death of owners

- owners bear unlimited liabilities

liable for all of the firm's debt without limit

owners use or sell their personal assets to pay off the unsettled debts

Firm -> separate legal entity

- separate legal existence from its owners

- firm enter into contracts, sued, and being sued

- will not be closed upon withdrawal/death of owners

- owners bear limited liabilities

not liable for the firm's debt that is more than their investments

no need to sell personal assets to pay of the unsettled debts

Forms of business ownership

Sole proprietorship

- owned by one person called the sole proprietor

- not a separate legal entity, owner bears unlimited liability

- limited sources of capital

- manged by owner

- e.g. a one-man-owned grocery store

Partnership

- 2/+ owners (partners)

- not a separate legal entity, 1/+ partner bears unlimited liability

- limited sources of capital

- bound by decisions made by the partnership, responsible for consequences of agreement violation

- e.g. a law firm and an audit firm

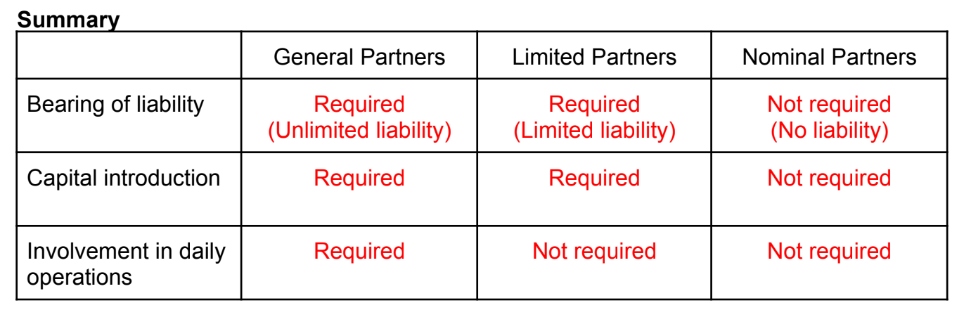

Types of partners

General partners

- will invest money

- bear unlimited liability

- will involve in daily operations and management

Limited Partners

- will invest money

- bear limited liability

- will not involve in daily operations and management

Nominal Partners

- will not invest money

- bear zero liability

- will not involve in daily operations and management

- providing professional advice.

- enhancing the firm’s reputation. Their reputation helps promote the partnership’s business.

- strengthening business linkages.

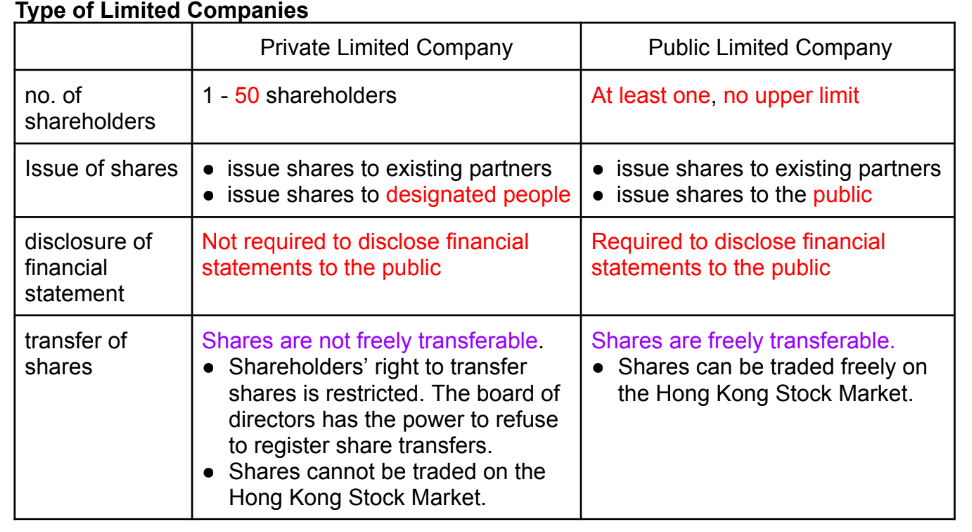

Type of limited companies

Pros/Cons of different forms of business ownership

Sole Proprietorship

- Low setup cost

- Efficient and flexible operations

- Sole claim of profits

- Lower profit tax rates

- Easy transfer of ownership

- Not a separate legal entity

- Unlimited Liability

- heavy workload

Partnership

- Wider sources of capital

- More management skills

- Sharing of work and business risks

- Lower setup cost (compared w/limited company)

- Lower efficiency and flexibility

- Hard transfer of ownership

- Not a separate legal entity

- Unlimited Liability

- Limited sources of capital

Limited Company

- Separate legal entity

- Limited liability

- Wider sources of capital

- Large-scale operations

- Complicated set-up procedures

- High setup costs

- Higher profit text rates

- Lower efficiency and flexibility

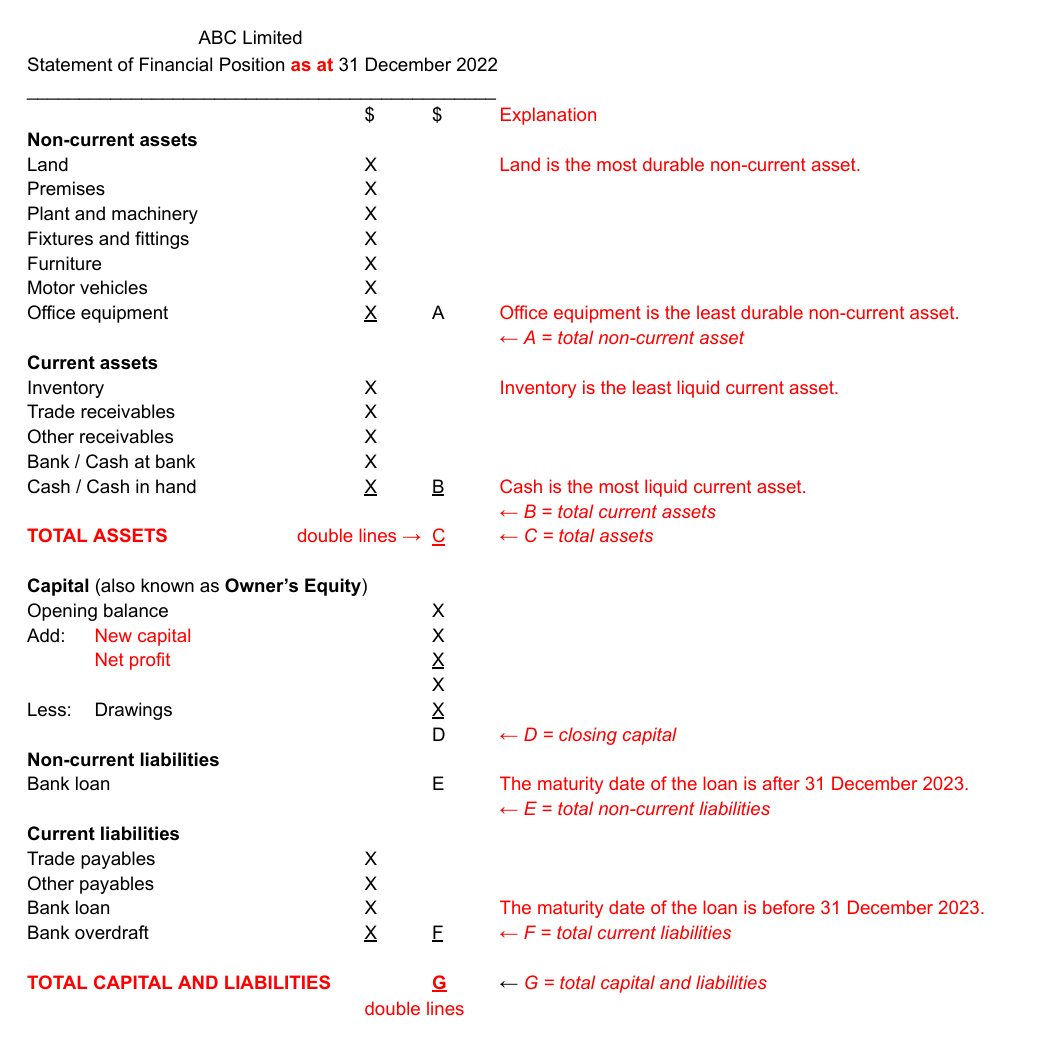

Assets = Capital + Liabilities

Current Assets

- Cash

- Expected to be converted to cash within the next accounting year

Non-current Assets

- Not current Assets

- Needed for operations of the business

- e.g. Furniture, Fixtures/Fittings

Current Liabilities

- Liabilities that are to be repaid within the next account year

- e.g. Bank Overdraft, Interest/Trade payable

Non-current Liabilities

- Liabilities that are will not be repaid within the next accounting year

Assets = Liabilities + Capital + (Revenue - Expense) - Drawings

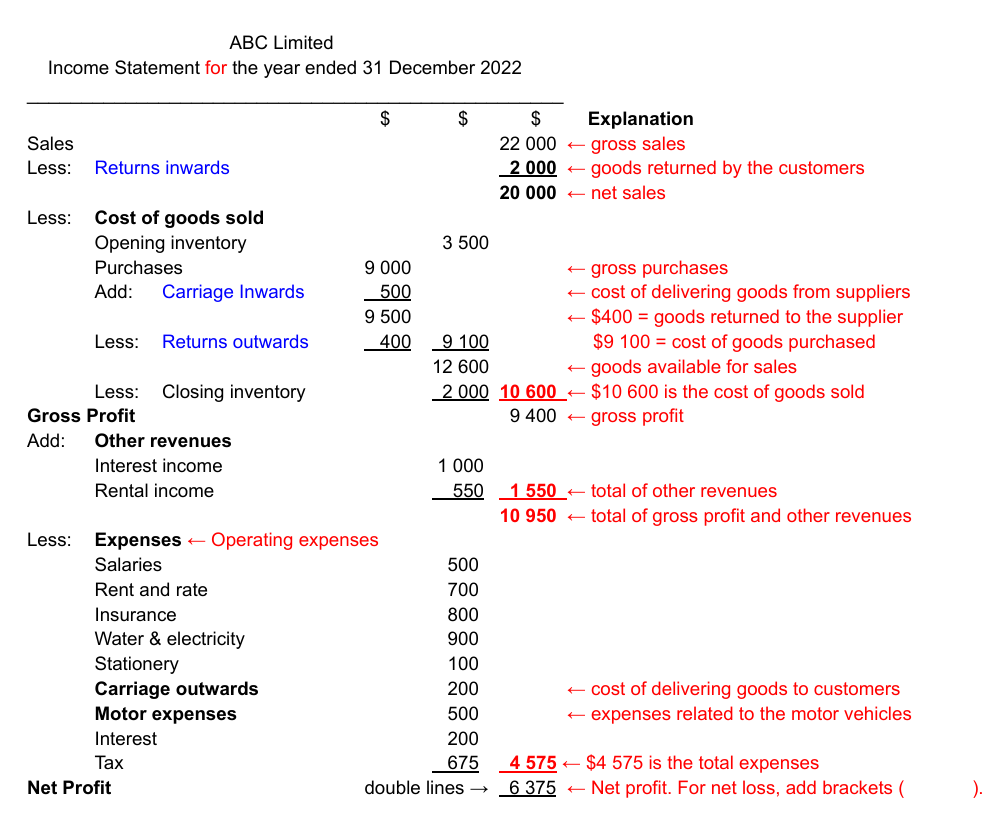

Revenue - Expensive = cost

Revenues

- Sales Revenue

- Interest Income

- Rental Income

Expenses

- Costs of goods sold

- insurance

- carriage in/outwards

- rent

- salaries

All money related: Capital

- e.g. Rent, resources supplied by owners

- anything money related that is not linked to a physical object or bank

Financial Statement

- Net sales = Sales - returns inwards

- Costs of Goods Sold = Opening inventory + costs of goods purchased - closing inventory

- Costs of goods purchased = purchases + carriage inwards - returns outwards

- Gross Profit = net sales - cost of goods sold

Financial Statement

Non-current assets

Durability: most to least

Current assets

Liquidity: least to most

Liabilities

No specific order

Closing Capital = Opening Capital + Net Profit - Drawings